A “return to normalcy,” a return to the way of life before World War I, was U.S. presidential candidate Warren G. Harding’s campaign promise in the election of 1920. Republican Harding won the election, and for nearly a decade it seemed that capitalist normality had indeed returned. The “Roaring Twenties” marked a period of relative prosperity, a downturn in labor militancy, and a soaring stock market.

In Europe, the shock waves set off by the Russian Revolution of October 1917 subsided and the capitalist ruling classes—with the crucial help of reformist “socialists”—succeeded in putting down the numerous uprisings and restoring relative political stability. Except for the British General Strike of 1926, largely the result of deflation brought on by an ill-fated attempt by the Bank of England to return the pound to its pre-war gold value, life on that continent also returned more or less to “normal.”

End to ‘quantitative easing’

On Oct. 29, the exact anniversary of the “Black Tuesday” 1929 stock market crash, the Federal Reserve Board, which sets U.S. monetary policy, announced it was ending its “quantitative easing” program as of Nov. 1.

Over six years and three separate QE rounds, the “Fed” bought some $3.5 trillion in government and mortgage bonds to keep interest rates low, put bank balance sheets on a more solid footing, rejuvenate the housing market, and encourage investment. It paid for these bonds with the electronic equivalent of newly printed dollars. Since many if not most of the securities purchased were owned by the biggest banks, the result was a huge buildup of bank reserves over and above the amounts legally required in the banks’ accounts at the Fed.

Fearing the inflationary effects if this avalanche of newly created paper money made its way into the economy through bank lending—potentially amounting to some multiple of the excess reserves based on the way the fractional reserve banking system works—the Fed began paying 0.25 percent interest on the reserves while leaning on the banks to tighten their lending standards.

The aim was to avoid a new speculative frenzy like the early to mid-2000s housing “bubble.” That bubble burst as a result of the sub-prime crisis of 2006-2008, hitting oppressed communities especially hard. As credit froze up and interest rates soared, the general overbuilding of housing and overproduction of most other commodities relative to demand backed by the ability to pay led to millions losing their jobs and their homes in the “Great Recession.”

The Fed steadily tapered its bond buying program this year from an initial $85 billion per month in an effort to get back to a more “normal” monetary policy. The central bank wound up QE with the purchase of $15 billion in assets in October.

The amount purchased in this latest round of QE, known as QE3, added up to $1.6 trillion, and the Fed’s balance sheet is now close to an unprecedented $4.5 trillion, compared to around $800 billion prior to the Great Recession.

Stock market gyrations

A near crash of the stock market on Oct. 15 (down 460 points on the Dow at one point) raised the possibility that the Fed might delay its planned ending of QE3 until December or beyond. This idea was voiced in a surprise interview on Bloomberg News the very next day by St. Louis Fed President James Bullard. But, with the market apparently stabilized in the days that followed, the central bank decided to move ahead and terminate the program.

With Fed bond buying ended, markets will now focus on when the central bank will raise its “policy rate,” the so-called federal funds rate charged when banks lend each other excess reserves overnight. The Fed has historically been able to raise and lower this rate by buying or selling short-term securities. Whether the Fed will have as much control of this rate in the future in view of the mountain of excess reserves that now exist is a question, though Fed Chair Janet Yellen and her predecessor Ben Bernanke have repeatedly stated that the central bank has “the tools” needed to get the job done.

There are sharp divisions among Fed officials on the timing of the first rate hike, reflecting—not surprisingly—differences in their assessments of the likely course of the economy. In the latest official Fed statement, however, the committee’s near-unanimous consensus is that “it likely will be appropriate to maintain the 0 to 1/4 percent target range for the federal funds rate for a considerable time. …”

Biggest banks bailed out

The first round of QE, which began Nov. 1, 2008, along with setting up emergency loan facilities and extending massive loan guarantees, saved the biggest banks from collapse. The huge infusion of liquidity no doubt saved the entire credit system and the rest of the economy from a devastating collapse as well. It doesn’t appear, however, that the subsequent two rounds actually did much to spur economic recovery, which has remained sluggish.

The real precondition for a vigorous upturn is liquidation of more of the overproduction that was built up in the period preceding the Great Recession. Progress has been made in this regard, especially in shrinking excess inventories—commodity capital—and the U.S. industrial cycle has transitioned from the depression/stagnation phase to the phase of what Marx called “average prosperity.” A precondition for average prosperity turning into a new “boom” is the elimination of more excess capacity in industry and stepped-up investment by corporations to expand their productive capacity.

Once that happens, we will again be “off to the races” towards a new boom, in which rapidly increasing production once again outruns a more slowly growing market. Even with renewed expansion of credit, demand will prove to be insufficient for all commodities produced to be sold at a profit, and the boom will turn into another bust. If the current industrial cycle follows its usual course, the next crisis would be due around 2017.

A return to ‘normalcy’ in the cards?

This would be the best-case scenario for a return to economic “normalcy.” But it isn’t hard to envision another outcome.

Central bank efforts to further ease monetary conditions in the aftermath of a severe crisis like the Great Recession have little influence. Once the crisis proper passes, monetary conditions are already greatly eased, with idle hoards of cash building up in banks and industrial corporations causing interest rates to plunge. On the other hand, tightening of monetary conditions by the central bank during an economic upturn can have quite negative consequences, aborting an upturn before a boom gets underway.

This is exactly what the Federal Reserve did in 1937 during the New Deal administration of Franklin Delano Roosevelt, when it doubled reserve requirements for big banks and took other measures to restrict credit. The administration itself moved to balance the federal budget by laying off large numbers of workers previously hired for public works projects. Social Security taxes were newly instituted, with benefits delayed for several years, further tightening government fiscal policy.

Fed officials feared that the 40 percent devaluation of the dollar that Roosevelt had carried out earlier, and the rise of wages resulting from the militant labor upsurge of the mid-1930s, would spark serious inflation. The ruling class as a whole also wanted to blunt, and if possible roll back, “labor’s giant step” toward organization of industrial workers into the CIO. The net result of these measures was the severe “Roosevelt recession” of 1937-1938, causing unemployment once again to soar.

Austerity-obsessed Europe

The European Central Bank and the various European Union governments are carrying out somewhat similar—that is, quite restrictive—policies today. The individual EU governments took on a great deal of debt as a result of bailing out their banks during the Great Recession. The U.S., thanks to the dollar being the world’s reserve currency, got away with printing large quantities when there was great demand for dollars as a means of payment during the crisis. However, the EU governments did not and do not enjoy that privilege.

The result was a major European “sovereign debt crisis” in which hedge funds and other money capitalists would only invest in newly issued government bonds at sky-high interest rates. This was especially the case for the so-called PIGS—Portugal, Italy, Greece and Spain. The Greek government had to partially default on its debt—the so-called haircut for bondholders—as part of a deal in which it was bailed out by the ECB and Germany.

The bond market, in effect, ordered all the governments to impose severe austerity if they wanted to ever again sell bonds at affordable rates of interest. That meant draconian cuts in social services, massive layoffs of government workers, cuts in pensions, and other “belt-tightening” measures—which the governments, regardless of ruling party or coalition, duly carried out.

Indeed, there was no alternative within the framework of continued capitalist rule. The policy has largely “worked,” though unemployment remains extremely high and the cuts in pensions and social services remain. Interest rates on government debt have fallen sharply. For example, the interest rate on 10-year euro area bonds has fallen more than 80 percent, to about 0.26 percent, while the rate on Italy’s bonds have fallen nearly 40 percent, to about 2.54 percent.

Greece’s 10-year interest rate also fell substantially over the past year, though in the last month it rose back up by about 25 percent—leaving a net decline of about 11 percent to a still unaffordable 7.60 percent. (tradingeconomics.com)

There is growing fear that Europe could fall into a deflationary spiral and a triple-dip recession if the ECB and EU governments don’t quickly ease up on monetary and fiscal policy. Adding to the threat are the sanctions the EU has imposed on Russia and Russia’s retaliatory response banning agricultural products from Europe. These tit for tat measures are the result of the U.S.-instigated right-wing coup in Ukraine in February, the subsequent defection of Crimea from Ukraine, and revolts by ethnic Russians in southeastern Ukraine.

Efforts on the part of Europe and Japan to escape deflation by easing credit conditions and taking other stimulative measures has the perverse effect of spreading deflation to the U.S. via the resulting flight into the dollar, causing the dollar’s gold value to rise (dollar price of gold to fall) while inflating bubbles in dollar-denominated assets such as U.S. stocks and bonds. These destabilizing effects are likely to be magnified now that the Federal Reserve has ended its dollar printing spree.

If Europe as a whole were to fall into a new recession, with China’s economy slowing down, the Ebola crisis in West Africa possibly spiraling out of control, and deflation spreading to the U.S., a new worldwide downturn could hit, perhaps as soon as next year.

Or, given the inherent instability of the dollar system and the huge pile of excess reserves in the banking system, there could suddenly be the opposite outcome—those reserves could be drawn into the economy through increased bank lending, setting off an inflationary spiral that would also inevitably end in a new recession when the Federal Reserve was forced to raise interest rates to save the dollar.

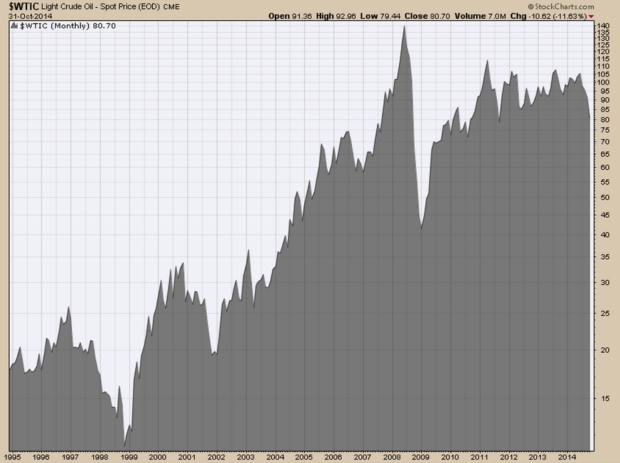

Behind the drop in oil prices

The slowdown in China and the pronounced economic weakness plaguing Europe combined with the rising value of the U.S. dollar against both the euro and gold–partly the result of a flight to safety by investors out of the euro and other weak currencies into the dollar—has pushed prices of primary commodities, all denominated in dollars, into a pronounced downtrend. A Reuters/Jefferies index of primary commodity prices has dropped from a level of 475 in October 2008 to about 275 now, a drop of about 42 percent. The price of copper, in particular, has fallen from around $4.50 per pound in February 2011 to around $3 currently, a drop of more than 30 percent.

As everyone who drives a car knows, oil and gasoline prices have also fallen sharply. An additional factor pushing these prices down has been the “fracking” boom in the U.S. According to an Oct. 26 McCatchy article, the U.S. in 2008 produced about 5 million barrels per day and imported about 60 percent of the oil it consumed. By this past April, U.S. production had reached 8.4 million barrels a day, with imports at the lowest level in nearly 20 years. (mercurynews.com)

Meanwhile, Saudi Arabia and other major oil producers have been reluctant to cut back on their production, setting off something of a price war. Since its peak of around $147 in July 2008, the price of light crude oil has fallen to about $80 currently, a drop of some 45 percent. Just since August of this year, the oil price has fallen nearly 30 percent.

The plunge in oil prices has led some analysts on the left to mistakenly conclude that the U.S. has been manipulating prices down in order to “punish” energy-exporting countries targeted for regime change, in particular Russia, Iran and Venezuela. While the price drop has undoubtedly undermined those economies, it has also adversely impacted the strategically important U.S. fracking boom.

If prices were to drop much more, the profits of the energy companies involved in fracking and other high-cost extraction of oil and gas would be wiped out and production would drop precipitously—eliminating any near-term prospect of U.S. energy independence and increased oil, gas and coal exports.

On the other hand, declining prices of oil and other imported commodities are beneficial to the U.S. economy in a way analogous to a tax cut for both corporations and individual consumers. For the former, production and distribution costs are reduced, boosting profits. For the latter, less money spent on gasoline, heating oil and (possibly) electricity means more money available for other purchases.

On balance, though, leaders of the U.S. empire would undoubtedly like to see higher, not lower, oil prices.

No return to ‘normalcy’

A situation has developed in the world economy that is reminiscent of the late 1990s when crises in Thailand and other “emerging economies” touched off a panicky flight to safety by investors into dollar-denominated financial assets. The extended period of low interest rates that resulted led first to the “dot com” stock market bubble, which ended in a crash, and then set off the housing boom that ended a few years later in a bubble that burst, another stock market crash, a near collapse of the entire banking system, and a severe crisis of overproduction. This time around, it is mainly developed Europe, not developing countries, causing panicked moves into the dollar, but the outcome could be similar even if it takes a different form.

In view of the chaos and multiple crises capitalist governments around the world are now grappling with—in some areas like the Middle East, these have actually resulted from interventions by the U.S. and/or its proxies—it seems clear that the Federal Reserve’s hoped-for return to “normalcy” is unlikely, to say the least. Even a brief stretch of relative peace and prosperity like the 1920s in the United States seems out of reach.

Instead, the prospect is for continued turbulence in the financial markets and more war and economic insecurity. This is the future that capitalism offers. It needs to be abolished, and that will take a new mass upsurge—this time a revolutionary upsurge of all the oppressed led by the working class.